While tourist classes once existed and the amount of the tourist tax depended on the location of the accommodation facility, this was changed with the adoption of the Tourist Tax Act in 2019.

It was determined what the minimum and maximum tourist tax amounts are for each type of accommodation (household accommodation, campsites, Robinson-style accommodation, etc.), while the decision on the exact amount of the tourist tax is made by the county assemblies for each city or municipality within their area individually. The main season period was also defined as the period from 1 April to 30 September, when the tourist tax may be higher, while during the rest of the year it may be lower.

Accommodation providers operating through a trade business or company

For every overnight stay, the guest pays the tourist tax to the accommodation provider. It is prescribed that during the main season (1 April – 30 September), the tourist tax amounts to a minimum of €1.33 per night and a maximum of €2.65 per night. During the rest of the year, the minimum amount per overnight stay is €0.93, while the maximum is €1.86.

The tourist tax is paid into the prescribed account on the 1st and 15th of each month for overnight stays achieved during that period. Certain groups, such as children and persons with disabilities, pay reduced amounts, which is described in detail in the Tourist Tax Act.

Accommodation providers offering household accommodation services and operating as individuals (so-called lump-sum taxpayers)

The tourist tax is paid in an amount that depends on the number of beds according to the official decision. The minimum amount that may be prescribed for a city or municipality is €46.45 per bed, while the maximum is €132.72. It is important to note here that all beds stated in the official decision are counted equally in the total number of beds, both main and auxiliary.

The tourist tax is calculated according to the number of beds, not according to the number of bed frames.

Many accommodation providers are also confused about whether the amount of the tourist tax is calculated according to the number of beds or sleeping places. The tourist tax depends on the number of sleeping places. Therefore, even if you have 2 double beds in an apartment, that is a capacity for 4 persons (4 beds), and that is the number multiplied by the defined tourist tax amount in order to obtain the final amount due.

Calculation example

For example, if you are a private accommodation provider paying lump-sum tax and you have capacity for 4 persons in main beds and 1 person in an auxiliary bed, and for your city or municipality the tourist tax has been set at €46.45 per bed (the lowest possible amount), on an annual basis you will pay a total of €232.25 (€46.45 × 5 beds), divided into three equal instalments with due dates on 31 July, 31 August and 30 September.

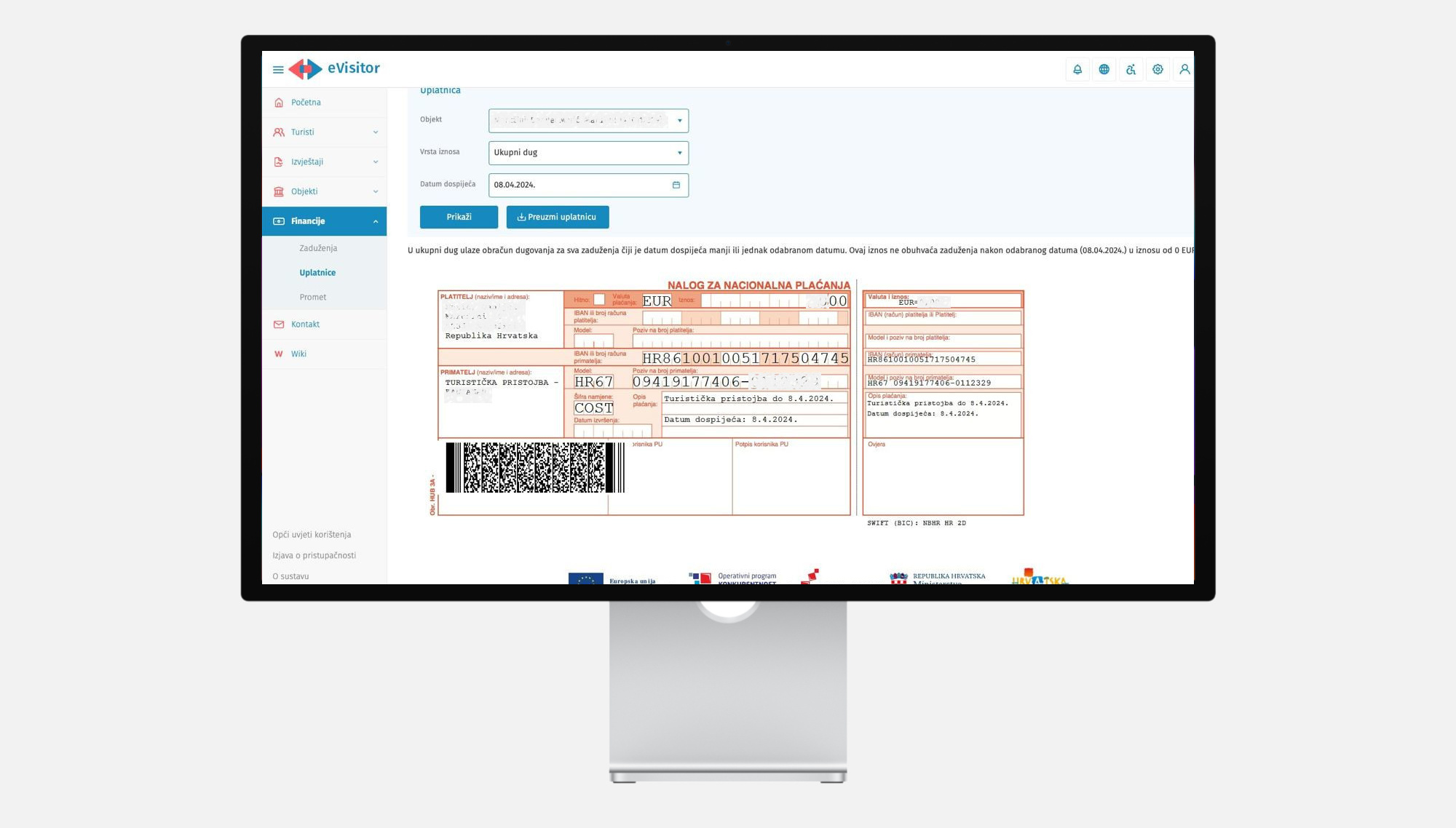

Note: tourist boards are not obliged to send payment slips, although some do. The accommodation provider independently retrieves the payment details in the eVisitor system.

We note again that the decision on the amount of the tourist tax may be changed every year, and if they wish to change the amount, the county assemblies are obliged to adopt such a decision by 31 January of the current year, for the amounts that will apply in the following year. To be certain of the tourist tax amount for your city or municipality, it is best to check with the competent tourist board or verify it in the eVisitor system, where the information is also regularly updated based on the decisions of the competent authorities.